Owning a rental property is a fantastic wealth-building strategy, but navigating the complex world of tax deductions can feel overwhelming. One of the most common questions landlords face is: how many years to depreciate plumbing for rental property? Getting this wrong could mean leaving money on the table or triggering an audit.

The short answer is that it depends on whether the plumbing is part of the original structure or a separate improvement. Generally, residential rental properties are depreciated over 27.5 years, but specific plumbing improvements might qualify for a shorter 15-year or even 5-year schedule under recent tax laws. In this guide, we will break down exactly how the IRS classifies plumbing, how to calculate your deductions, and strategies to optimize your cash flow.

The General Rule: 27.5-Year Residential Rental Property

For most landlords, the baseline for depreciation is the Modified Accelerated Cost Recovery System (MACRS). Under this system, the IRS views the entire residential rental building—including its structural components—as a single asset with a useful life of 27.5 years.

What Counts as “Structural” Plumbing?

If the plumbing was installed when the building was constructed, or if you replace major lines that are embedded in the walls or foundation, it is considered part of the building’s structure. This includes:

- Main water supply lines entering the home.

- Sewer lines connecting to the municipal system.

- Pipes hidden behind drywall or under concrete slabs.

Because these items are integral to the building’s existence, they must be depreciated over the same 27.5-year period as the rest of the property. You cannot separate them out to accelerate the deduction unless you meet specific criteria for “qualified improvement property,” which we will discuss later.

When Can You Depreciate Plumbing Over 15 Years?

This is where many landlords miss out on significant tax benefits. The Tax Cuts and Jobs Act (TCJA) introduced a category called Qualified Improvement Property (QIP). While QIP primarily targets commercial real estate, there are nuances for multi-family rentals and specific scenarios where interior improvements might qualify for a 15-year recovery period instead of 27.5 years.

However, for typical single-family residential rentals, the 15-year rule is less common for plumbing unless it is part of a larger rehabilitation project that qualifies under specific historic preservation credits or non-residential portions of a mixed-use property.

Key Distinction:

- Residential Rental (Single Family/Duplex): Typically 27.5 years.

- Commercial/Mixed-Use Interior Improvements: Potentially 15 years (QIP).

Note: Always consult a CPA to determine if your specific property mix qualifies for QIP status, as misclassification is a common audit trigger.

The 5-Year Exception: Personal Property & Appliances

Not all plumbing-related items are tied to the building. The IRS allows certain assets to be classified as personal property rather than real property. These items have a much shorter depreciation schedule of 5 years.

What Plumbing Items Qualify for 5-Year Depreciation?

If the plumbing component is not permanently affixed to the structure or can be removed without damaging the building, it may qualify. Examples include:

- Standalone Water Heaters: If not built into the wall structure.

- Water Softeners: Standalone units.

- Sump Pumps: Portable or easily replaceable units.

- Appliances with Plumbing Hookups: Dishwashers and washing machines (though these are often grouped under appliances rather than plumbing).

By correctly identifying these items as personal property, you can write off their cost much faster, improving your early-year cash flow.

Bonus Depreciation: Accelerating Your Deductions

One of the most powerful tools in a landlord’s arsenal is Bonus Depreciation. This provision allows you to deduct a large percentage of the cost of qualifying property in the first year it is placed in service.

Current Bonus Depreciation Rates

Under current tax laws, bonus depreciation is phasing down. However, for qualified property (like the 5-year personal property mentioned above), you may still be able to claim a significant portion immediately.

- 2023-2024: 80% bonus depreciation.

- 2025: 60% bonus depreciation.

- 2026: 40% bonus depreciation.

Important: Bonus depreciation generally applies to personal property (5-year items) and certain land improvements, not to the 27.5-year structural plumbing. Therefore, segregating your costs between “structural plumbing” and “plumbing fixtures/appliances” is critical.

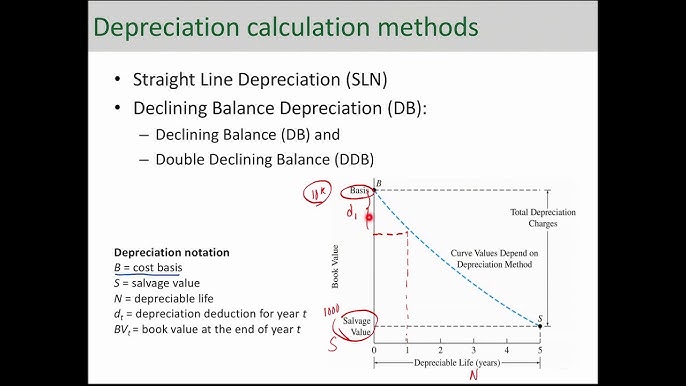

Step-by-Step: How to Calculate Your Depreciation

Calculating depreciation correctly requires attention to detail. Follow these steps to ensure accuracy:

- Determine the Basis: Identify the total cost of the plumbing work. Include materials, labor, permits, and any associated fees.

- Segregate Costs: Break down the invoice. Separate structural pipes (27.5 years) from standalone fixtures like water heaters (5 years).

- Identify the Placed-in-Service Date: Depreciation begins when the property is ready and available for rent, not necessarily when the work was completed.

- Choose Your Method: Most landlords use the General Depreciation System (GDS) with the Mid-Month Convention for residential property. This assumes the property was placed in service in the middle of the month, regardless of the actual date.

- Apply the Formula:

- Annual Depreciation = Cost Basis / Recovery Period

- Example: $5,500 structural plumbing / 27.5 years = $200 per year.

For more detailed information on MACRS tables, you can refer to the official IRS Publication 946 or general accounting principles found on Wikipedia’s MACRS page for a broad overview of the system’s history and structure.

Repair vs. Improvement: A Critical Distinction

Before you depreciate, ask yourself: Is this a repair or an improvement?

| Feature | Repair (Deduct Immediately) | Improvement (Depreciate) |

|---|---|---|

| Definition | Keeps property in normal operating condition. | Adds value, prolongs life, or adapts to new use. |

| Example | Fixing a leaky faucet. | Replacing all galvanized pipes with PEX. |

| Tax Treatment | 100% deductible in current year. | Must be capitalized and depreciated over time. |

| Impact | Lowers taxable income now. | Lowers taxable income over 5–27.5 years. |

The IRS uses the BAR Test to determine if something is an improvement:

- Betterment: Does it improve the property beyond its original state?

- Adaptation: Does it adapt the property to a new use?

- Restoration: Does it restore the property to a like-new condition?

If you answer “Yes” to any of these, it is likely an improvement that must be depreciated.

FAQ Section

1. Can I expense plumbing repairs under the Safe Harbor for Small Taxpayers?

Yes. If your total annual repairs and maintenance costs do not exceed the lesser of $2,500 or 2% of your unadjusted basis in the building, you may be able to deduct them immediately rather than depreciating. This is known as the De Minimis Safe Harbor.

2. Does replacing a water heater count as plumbing?

A standalone water heater is typically classified as personal property with a 5-year depreciation life, not structural plumbing. This allows for faster write-offs and potential bonus depreciation.

3. What happens to depreciation when I sell the property?

When you sell, you must recapture the depreciation you claimed. This is taxed at a maximum rate of 25% for residential real estate. Properly tracking your plumbing depreciation helps you anticipate this tax liability.

4. Can I use Section 179 for plumbing improvements?

Section 179 is generally reserved for business equipment and personal property. While you might use it for a standalone water heater (personal property), you cannot use Section 179 for structural plumbing integrated into a residential rental building.

5. Do I need an engineer to segregate costs?

For small projects, a detailed contractor invoice is usually sufficient. For large renovations exceeding $100,000, a cost segregation study by a professional engineer or CPA is highly recommended to maximize tax benefits legally.

6. How does the mid-month convention affect my first year?

If you place the property in service in June, you only get half a month’s depreciation for June, plus full months for July–December. This reduces your first-year deduction slightly but standardizes calculations for all taxpayers.

Conclusion

Understanding how many years to depreciate plumbing for rental property is essential for maximizing your return on investment. While structural plumbing generally falls under the 27.5-year rule, identifying opportunities to classify items as personal property (5-year) or leveraging bonus depreciation can significantly boost your cash flow.

Remember, the key to successful real estate investing isn’t just about collecting rent—it’s about keeping more of what you earn through smart tax strategies. Always keep detailed records, segregate your costs carefully, and consult with a tax professional who specializes in real estate.

Found this guide helpful? Share it with your fellow landlords on Facebook or LinkedIn to help them navigate their tax season with confidence!

Leave a Reply