Have you ever woken up to a mysterious wet spot in your yard or noticed your water bill skyrocketing without explanation? These could be signs of underground plumbing issues that require excavation—and the big question on every homeowner’s mind is: Is underground in house plumbing excavation covered by insurance? The answer isn’t always straightforward, but understanding your coverage can save you thousands of dollars.

What Does Homeowners Insurance Typically Cover for Plumbing?

Homeowners insurance policies vary significantly, but most standard policies follow similar guidelines when it comes to plumbing damage. Generally, insurance covers sudden and accidental damage rather than gradual deterioration or maintenance issues.

According to industry data from the Insurance Information Institute, water damage and freezing account for approximately 24% of all homeowners insurance claims, making plumbing issues one of the most common reasons homeowners file claims.

Covered Scenarios:

- Sudden pipe bursts due to freezing temperatures

- Accidental damage from external forces (like tree roots breaking pipes)

- Water damage resulting from covered plumbing failures

- Emergency excavation necessary to access and repair covered damage

Not Typically Covered:

- Gradual leaks that develop over time

- Wear and tear from aging pipes

- Poor maintenance or neglect

- Pre-existing conditions known before policy inception

When Is Underground Plumbing Excavation Covered?

The key factor determining coverage is the cause of the damage, not necessarily the location of the pipes. Let’s break down specific scenarios:

Sudden and Accidental Damage

If a pipe suddenly bursts due to freezing weather or an unexpected event, most policies will cover both the repair costs and necessary excavation. For example, if winter temperatures drop below freezing and cause your main water line to crack, your insurance typically covers:

- The cost to excavate and access the damaged pipe

- Repair or replacement of the broken section

- Restoration of landscaping or driveways disturbed during excavation

External Force Damage

Damage caused by external factors like tree root intrusion, ground shifting, or accidental damage during construction may be covered depending on your policy terms. Some insurers consider tree root damage as “gradual” while others view it as sudden if it causes immediate failure.

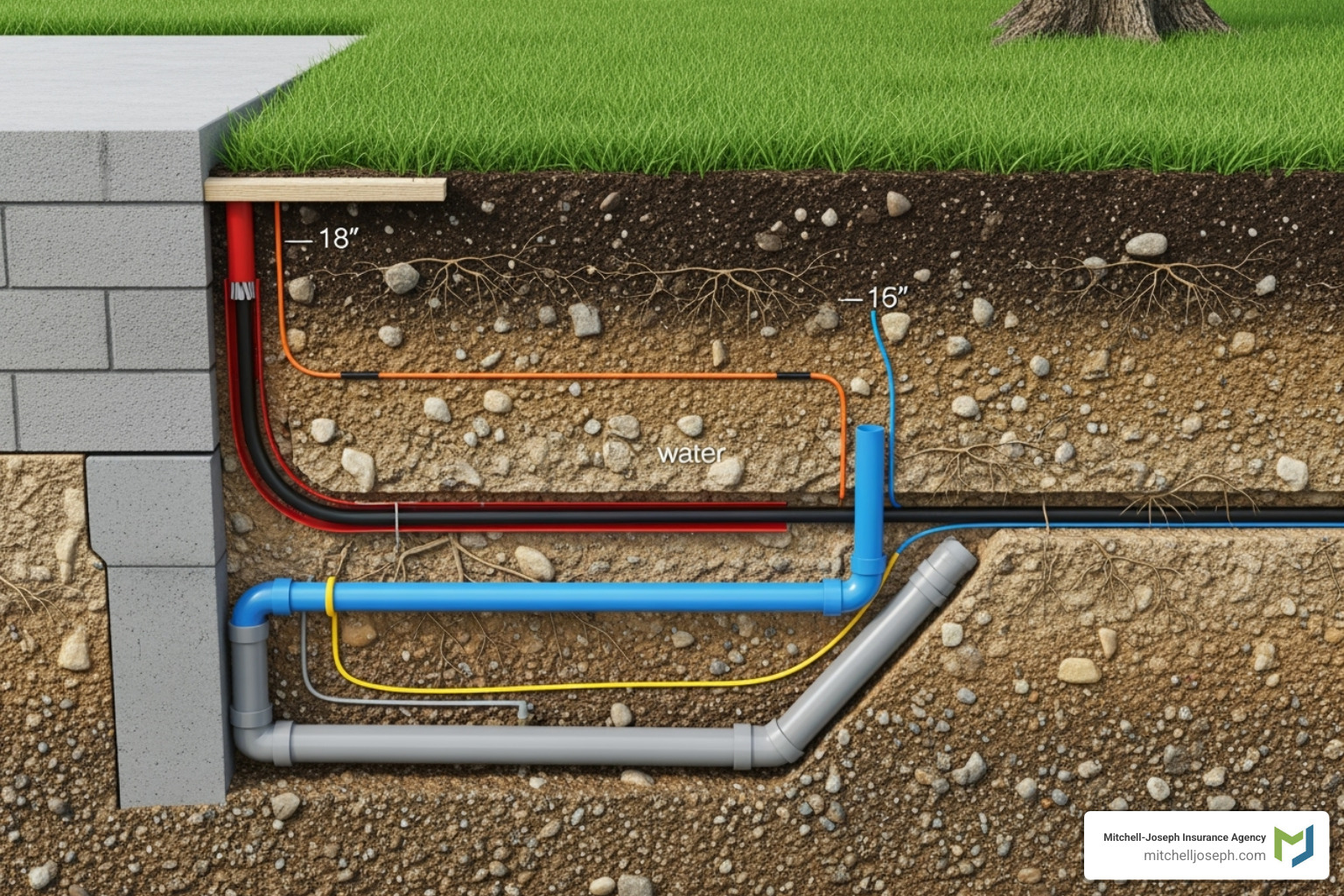

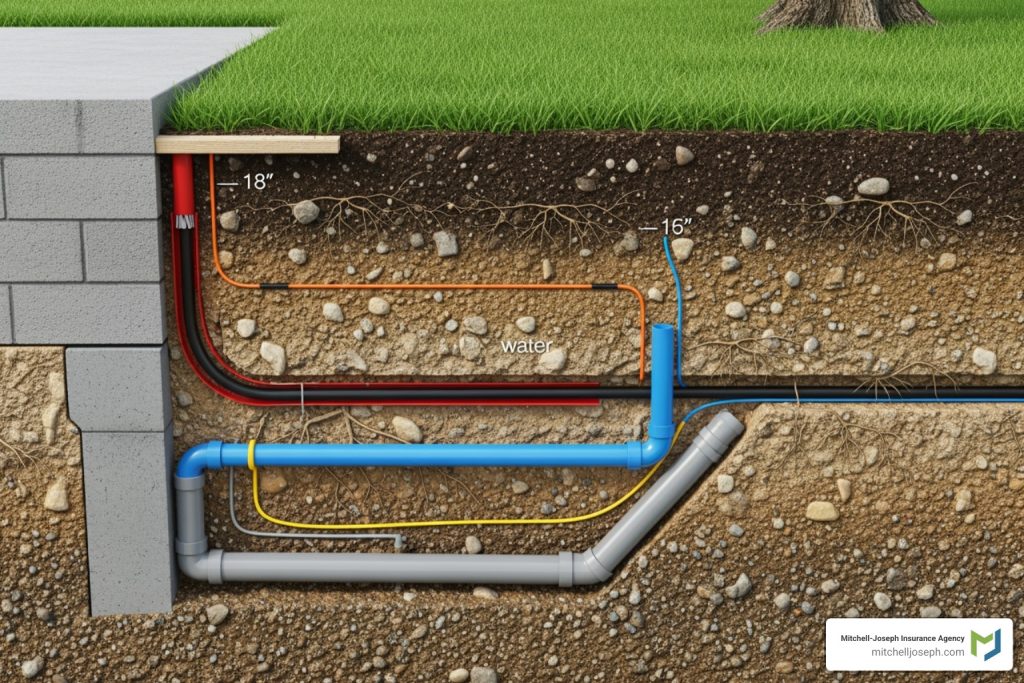

Service Line Coverage

Many homeowners don’t realize that standard policies often exclude damage to utility lines outside the home’s foundation. However, you can purchase service line coverage as an endorsement, which typically costs $50-$100 annually and covers:

- Water supply lines

- Sewer lines

- Electrical cables

- Internet/phone lines

This coverage usually includes excavation costs up to $10,000-$25,000 depending on your policy limits.

What Factors Affect Insurance Coverage for Excavation?

Several variables influence whether your claim will be approved:

Policy Type and Endorsements

- HO-3 policies (most common) provide broad coverage but have specific exclusions

- HO-5 policies offer more comprehensive protection

- Additional endorsements can expand coverage to include service lines

Age and Condition of Plumbing

Insurance companies may deny claims if they determine the damage resulted from:

- Pipes older than 50 years without recent inspection

- Known issues that weren’t addressed

- Lack of proper maintenance records

Documentation and Evidence

Successful claims require thorough documentation:

- Photos of the damage before and after excavation

- Professional plumber’s assessment report

- Receipts for emergency services

- Proof of regular maintenance

How to Determine If Your Policy Covers Underground Excavation

Follow these steps to verify your coverage:

- Review your policy declarations page – Look for “service line coverage” or “underground utilities” mentions

- Check for exclusions – Read the exclusions section carefully for language about “gradual damage” or “wear and tear”

- Contact your insurance agent – Ask specific questions:

- “Does my policy cover excavation costs for underground pipe repairs?”

- “What causes of damage are covered versus excluded?”

- “Do I need additional endorsements for service line protection?”

- Document everything – Take photos, keep receipts, and maintain records of all communications

- Get multiple quotes – Before proceeding with excavation, obtain at least three estimates from licensed plumbers

Cost Comparison: With vs. Without Insurance Coverage

| Expense Item | Average Cost Without Insurance | With Insurance (after deductible) |

|---|---|---|

| Excavation labor | $1,500 – $4,000 | $500 – $1,500 |

| Pipe repair/replacement | $2,000 – $6,000 | $500 – $2,000 |

| Landscape restoration | $1,000 – $3,000 | $200 – $800 |

| Emergency service call | $200 – $500 | $0 – $100 |

| Total Range | $4,700 – $13,500 | $1,200 – $4,400 |

Note: Costs vary by region, severity of damage, and policy deductible amounts.

Tips to Prevent Underground Plumbing Issues

Prevention is always better than dealing with insurance claims. Here are proactive measures:

Regular Inspections

- Schedule professional plumbing inspections every 2-3 years

- Use camera inspection services to check underground lines

- Monitor water bills for unusual increases

Landscaping Considerations

- Plant trees at least 10 feet away from underground pipes

- Avoid heavy equipment near known pipe locations

- Use root barriers around vulnerable areas

Winter Protection

- Insulate exposed pipes before cold weather

- Keep garage doors closed to protect indoor lines

- Let faucets drip slightly during extreme cold

Know Your System

- Locate your main shut-off valve

- Understand where your service lines enter the property

- Keep updated diagrams of your plumbing layout

For more detailed information about homeowners insurance standards, you can reference Wikipedia’s article on homeowners insurance, which provides comprehensive background on policy types and coverage principles.

Frequently Asked Questions

Q: Does homeowners insurance cover the cost of digging up my yard to fix pipes?

A: Yes, if the underlying pipe damage is covered by your policy. Most insurers will pay for reasonable excavation costs necessary to access and repair covered damage. However, they won’t cover excavation for routine maintenance or gradual deterioration.

Q: What’s the difference between sudden damage and gradual damage in insurance terms?

A: Sudden damage occurs unexpectedly and immediately, like a pipe bursting overnight. Gradual damage develops slowly over time, such as small leaks that worsen gradually. Insurance typically covers sudden damage but excludes gradual damage because it’s considered a maintenance issue.

Q: How much does service line coverage typically cost?

A: Service line coverage usually costs between $50-$100 per year as an endorsement to your standard homeowners policy. This relatively small investment can save you thousands in excavation and repair costs if underground utilities fail.

Q: Will my insurance premium increase after filing a plumbing claim?

A: Possibly. Most insurers review claims history when renewing policies. A single small claim might not significantly impact your premium, but multiple claims within a few years could lead to higher rates or even policy non-renewal. Consider paying out-of-pocket for minor repairs if possible.

Q: What should I do immediately if I suspect underground pipe damage?

A: First, shut off your main water supply to prevent further damage. Document the situation with photos and videos. Contact a licensed plumber for assessment, then notify your insurance company before starting any repairs. Keep all receipts and communication records for your claim.

Q: Can I choose my own contractor for excavation work?

A: Yes, you generally have the right to choose your contractor. However, some insurance companies have preferred vendor networks that may offer discounted rates. Compare quotes from both preferred and independent contractors to ensure you’re getting fair pricing.

Conclusion

Understanding whether underground in house plumbing excavation is covered by insurance requires careful attention to your specific policy terms and the cause of damage. While sudden and accidental damage is typically covered, gradual deterioration usually isn’t. The key is knowing your coverage limits, maintaining proper documentation, and considering additional endorsements like service line coverage for comprehensive protection.

Remember, prevention through regular inspections and proper maintenance can help avoid costly repairs altogether. If you find this guide helpful, please share it with fellow homeowners on social media—knowledge about insurance coverage can save everyone from unexpected financial burdens.

Stay informed, stay protected, and don’t hesitate to contact your insurance provider with specific questions about your policy. Your peace of mind is worth the effort!

Leave a Reply